(Singapore, 23 Jan 2025)Asia-Pacific’s office sector offers compelling opportunities for value-add investments, according to Knight Frank Asia-Pacific’s latest outlook report, Charting new horizons – 25 trends shaping 2025. The report features its 25 key significant developments across sectors trends.

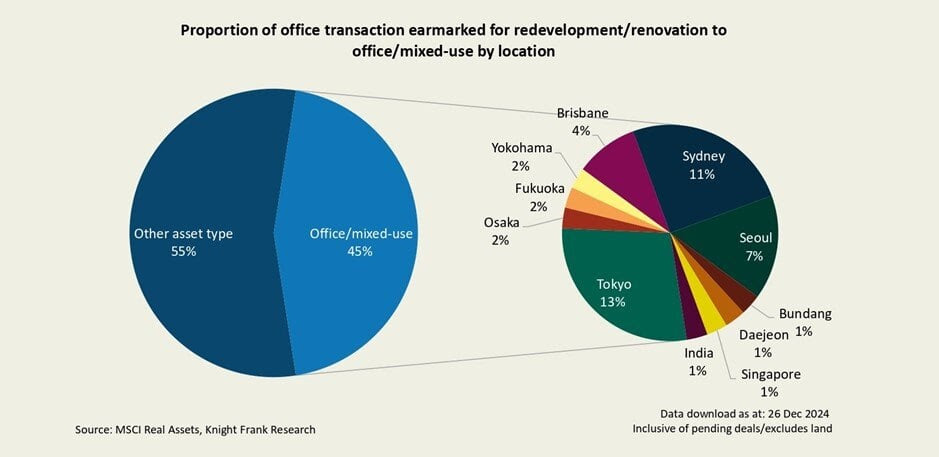

The report showed that 45% of office transactions earmarked for redevelopment or renovation focused on upgrading and enhancing office specifications in 2024. The issue of building obsolescence gained prevalence over the past year, as Grade B and lower-tier buildings face increasing challenges in leasing due to a growing ‘flight-to-quality’ trend among corporate occupiers. This shift presents significant investment opportunities in the value-add segment, particularly in revitalising older stock by incorporating ESG (environment, social and governance) and wellness features.

Christine Li, head of research, Asia-Pacific says, “The Asia-Pacific office sector is evolving into a two-tiered market, offering opportunities for value-add investors. This transformation is driven by the widening gap between outdated and premium office spaces, increasing focus on sustainability and ESG compliance, and mandatory stock market regulations. Consequently, we are witnessing a sustained demand for ESG-compliant office spaces.”

Neil Brookes, global head of capital markets, Knight Frank, says, “Despite ongoing challenges, we expect a steady recovery in the region as pricing stabilises, bid-ask spread narrows, and confidence grows. Investors are increasingly diversifying their portfolios with alternative real estate investments alongside traditional assets. Diverse market conditions and economies in the region offer opportunities for different investment strategies, requiring investors to remain adaptable and responsive in their strategic approaches to capitalise on the most attractive opportunities.”

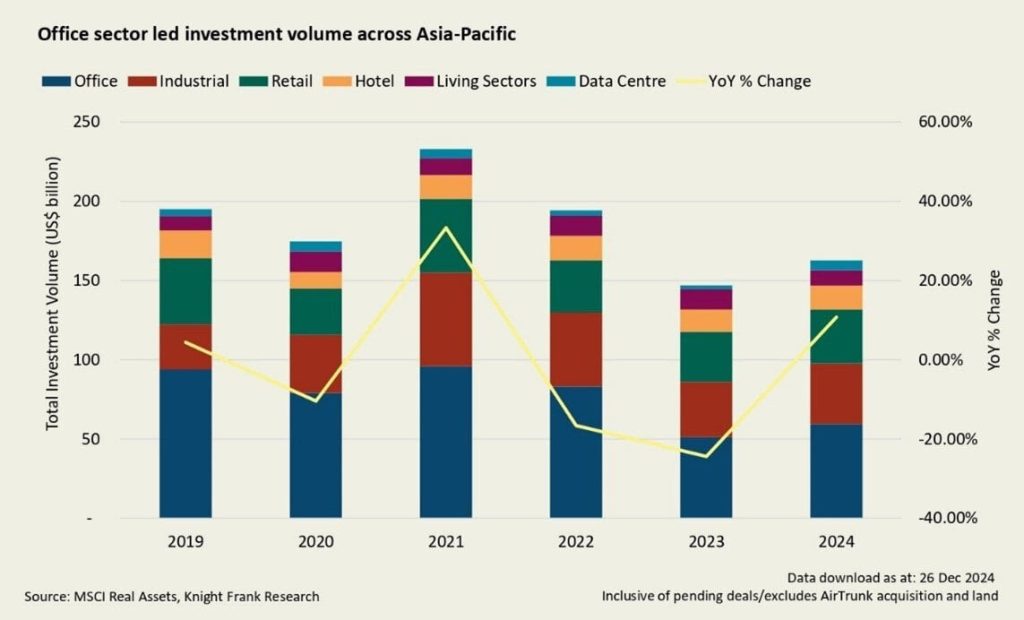

16% Rise in APAC office investment, first uptick in two years

The office sector led investment volume across Asia-Pacific. Annual investment volume in office assets grew 16%, the fastest growing asset class, to reach US$59.5 billion in 2024 from US$51.2 billion in 2023. This growth accounted for 37% of all capital received in the region’s real estate market.

A major draw of office assets in Asia-Pacific is the high occupancy rate compared with western counterparts. Utilisation rate averages to 80% in the region, far higher than the 65% recorded in major US cities and 70% in the UK and Europe.

Data centres lead alternative real estate amid shifting investor landscape

Investor appetite for defensive sectors remains strong, with data centres leading alternative real estate investments, despite anticipated rate cuts. Data centres have consistently ranked first in niche property type prospects, showcasing remarkable growth. In 2024, data centre investments reached US$6.3 billion (excluding the AirTrunk takeover) a 2.5-fold increase from US$2.5 billion in 2023. This trend is driven by persistent pricing expectation gaps and narrowing yield spreads, pushing investors towards assets that can meet their return targets.

Fred Fitzalan Howard, data centre lead, Knight Frank, says “Asia-Pacific offers significant investment opportunities in the data centre sector due to strong live supply growth and a persistent supply-demand imbalance. From 2018 to 2023, the region experienced a compound annual growth rate (CAGR) of 19% in live supply, as reported by DC Byte. Yet, the current supply remains insufficient to meet the demands of its vast population’s digital growth. Malaysia continues to lead as the top data centre hub in Knight Frank’s SEA-5 Data Centre Opportunity Index 2024, while emerging markets such as Chennai, Melbourne, and Bangkok show promising potential in this sector as Cloud Service Providers and AI companies diversify away from tier 1 data centre hubs.”

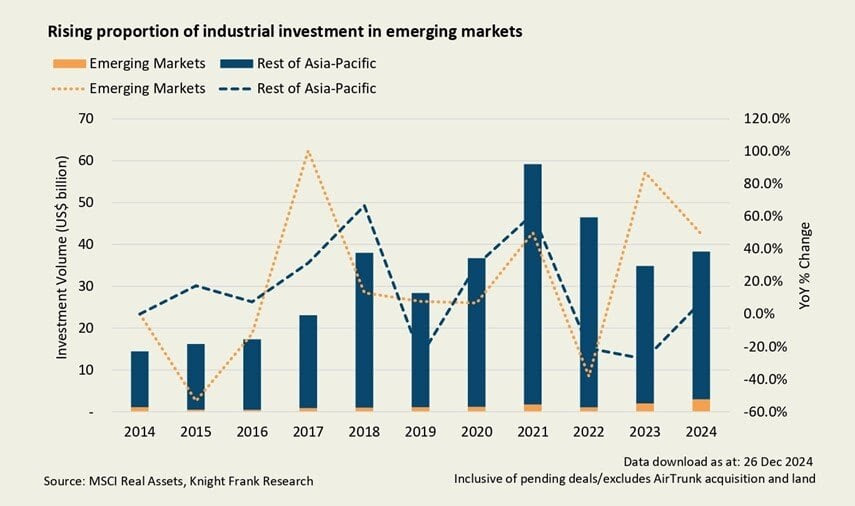

Emerging markets drive industrial asset growth amid global supply chain shifts

The industrial sector in emerging markets experienced remarkable growth, with total capital received for industrial assets reaching a record-breaking US$3.0 billion in 2024, marking a 50% increase from the previous year. This growth significantly outpaced the rest of Asia-Pacific, which saw only an 8% increase during the same period.

Vietnam emerged as a leading investment destination in the region, leveraging its strategic proximity to Chinese mainland and strong export growth. As Southeast Asia’s largest exporter, Vietnam’s exports grew rising from US$320 billion in 2019 to US$440 billion in 2023 at a CAGR of 8.2%, as noted by IHS Markit, driven by substantial foreign direct investment in manufacturing.